Global coal consumption will defy expectations

China and India, the world’s largest coal consumers, will consume much more coal than energy analysts predict

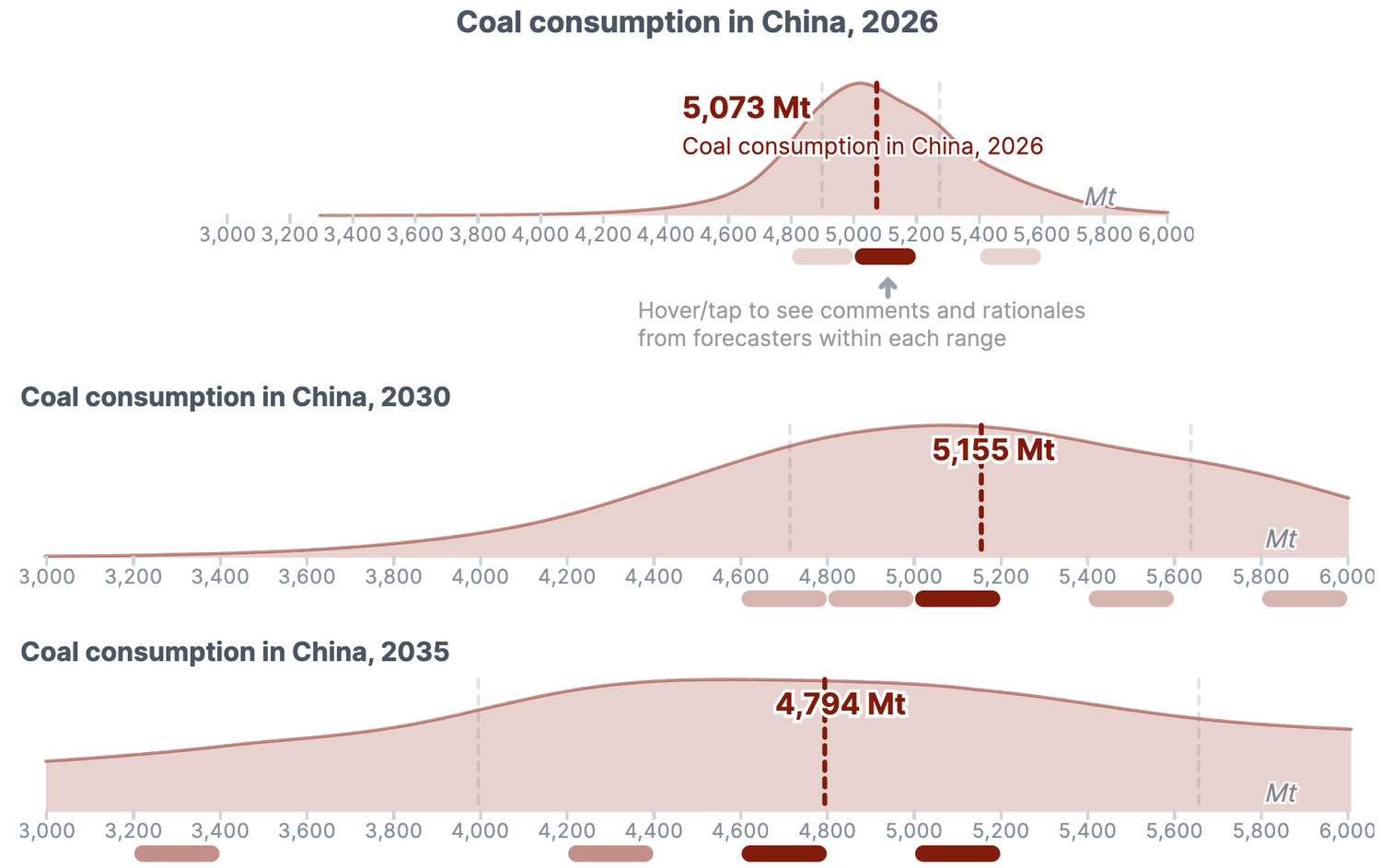

97% chance Chinese coal consumption in 2026 will be greater than IEA’s forecasted quantity

99% chance Indian coal consumption in 2026 will be greater than IEA’s forecasted quantity

Indian and Chinese coal consumption in 2035 likely to be at least 25% higher than analysts’ expectations

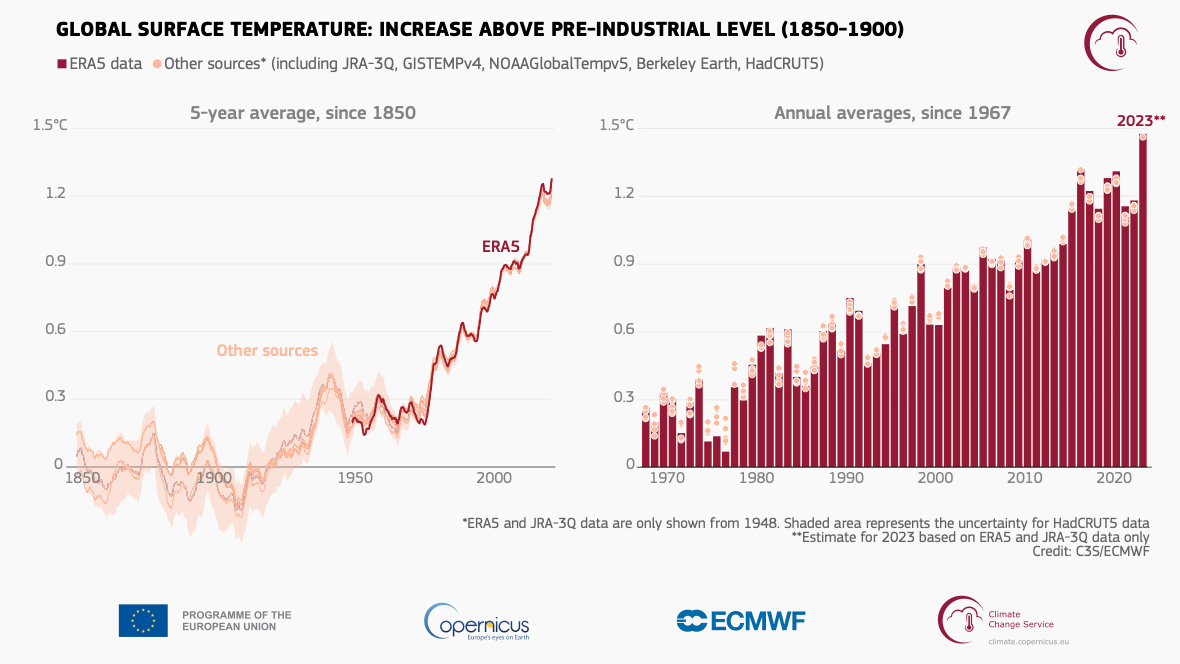

The flagship goal of the Paris Agreement, an international treaty signed nearly 7 years ago, was stated clearly in article 2: “[hold] the increase in the global average temperature to well below 2°C above pre-industrial levels and to pursue efforts to limit the temperature increase to 1.5°C above pre-industrial levels”. At the time, the world was 1°C warmer than it was over 1850–1900, and the five-year average temperate has increased nearly 0.3°C more since then.

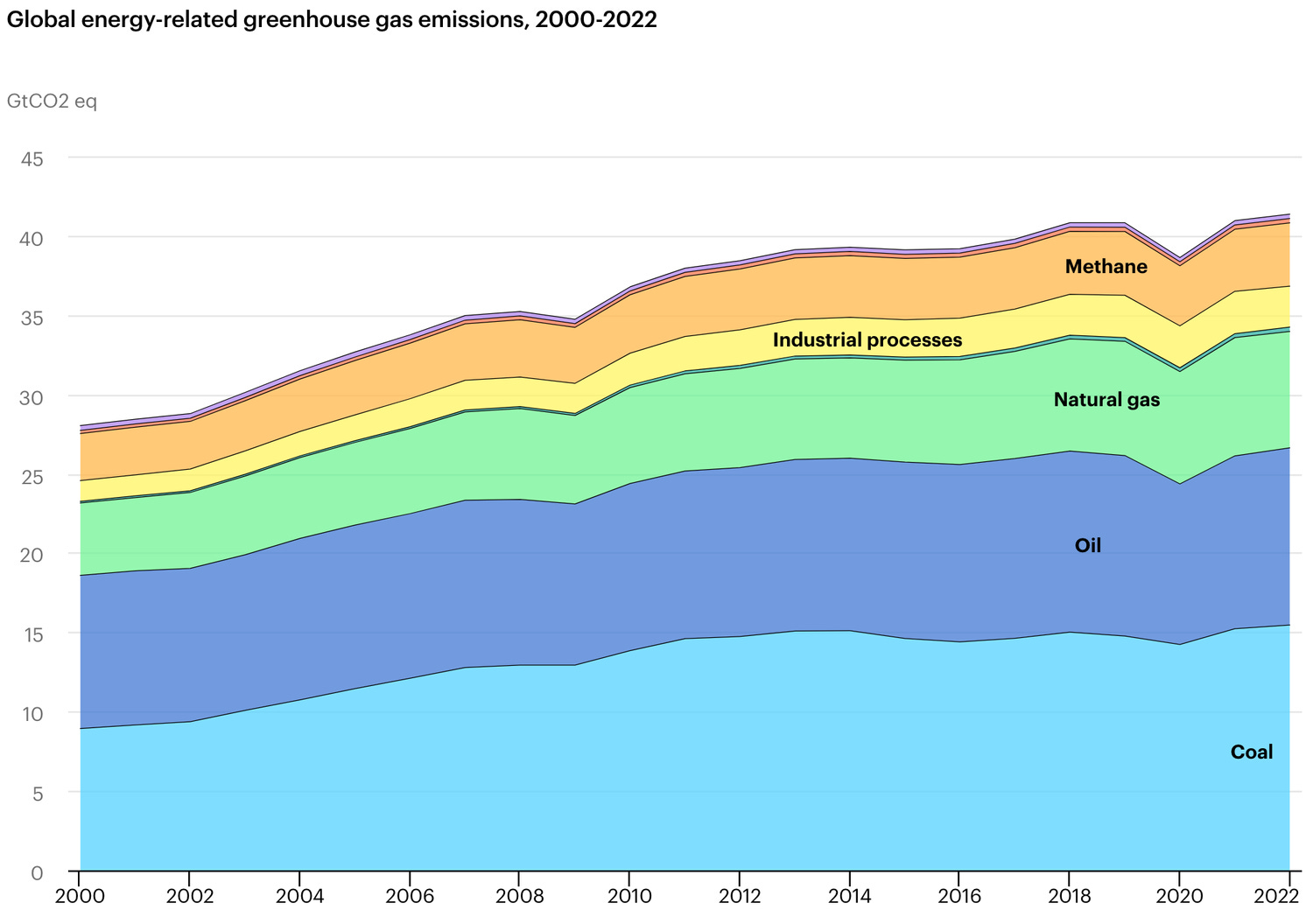

In order to keep the global average temperature below 2°C, greenhouse gas emissions will need to be rapidly reduced.

Coal is being phased out in advanced economies due to its high pollution levels, as it releases the most CO2 and local air pollutants per unit of energy produced during combustion compared to other energy sources. Despite that progress, it still remains the single largest source of greenhouse gas emissions globally.

The world's largest consumers of coal are China and India, respectively consuming 4.5 and 1.1 billion tonnes of the fuel in 2022. These two countries are the focus of this forecasting report as they together account for nearly 70% of global coal consumption.

China’s coal consumption

Coal is a significant contributor to China's greenhouse gas emissions, accounting for over 60% of the country's total emissions. This is due to both the combustion of coal for energy production and the emissions associated with its processing. The processing emissions are not insignificant; the United States Environmental Protection Agency estimates the methane emissions from Chinese coal mines was equivalent to the release of 660 million tonnes of carbon dioxide in 2020.

China's heavy reliance on coal is driven by its rapid economic growth and industrialisation over the past few decades. The country has vast coal reserves and has traditionally relied on coal as a cheap and abundant energy source.

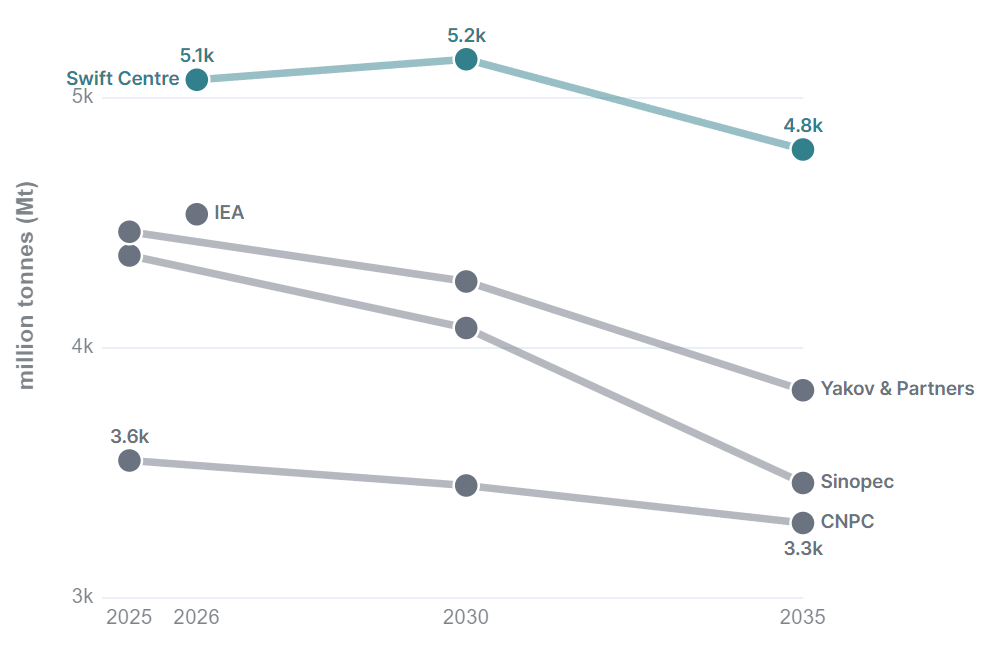

The IEA, widely regarded as the most authoritative voice on global energy trends, predicts that both global and Chinese coal consumption has peaked.

China Petroleum & Chemical Corporation (Sinopec), China’s largest oil and gas enterprise, similarly predicts Chinese coal consumption will start to decline soon, peaking around 2025. This reflects a delay in decarbonisation relative to previous industry forecasts. Coal consumption was expected to have peaked back in 2016, according to older predictions made by the China National Petroleum Corporation (CNPC), another major state-owned oil and gas company.

Smaller independent groups, such as Moscow-based consultancy firm Yakov and Partners, also forecast Chinese coal consumption to decline from 2025 onwards (albeit more slowly than China’s firms predict).

Our forecasters think this outlook is misguided.

Swift Centre’s top-performing generalist forecasters believe China’s coal consumption will remain higher for longer than any of these groups predicts.

The aggregate of the group’s forecasts suggests coal usage is highly likely to continue rising, and we find the IEA's claim that 2023 was China's "peak coal" year to be essentially implausible. Our median estimates of coal usage in China are 10% higher than the IEA's projections for 2026, 20% higher than Yakov & Partners' forecast for 2030, and a staggering 40% higher than Sinopec's prediction for 2035. The differences are even more pronounced when compared to the CNPC's 2018 projections.

Such strong divergence from other organisations is striking. Despite being an outlier, there are good reasons to expect our estimates to perform better than others on this matter. Our forecasters have a history of winning competitions, as they take a wide variety of information into account and are less prone to cognitive biases.

In contrast, predictions made by field experts without forecasting and calibration training suffer from a variety of preventable, systematic biases such as optimism bias and overconfidence bias. These lead to predictions that are biased towards their preferred outcome (in this case, low emissions), assuming that coal usage will be far below what past trends suggest. One forecaster pointed to the IEA’s track record as a clear example of this:

The IEA’s forecasting errors offer a remarkable consistency of about 2.8 percentage points per year. Adjusting for this error over the years gets me to a median estimate of 5,022 Mt in 2026.

The IEA forecasts China consuming 4,535 Mt of coal in 2026, while the aggregate of our forecasters’ probability distributions suggests that there is a 97% chance that it will be greater.

For 2030, we believe there is a 95% chance China’s coal consumption will be greater than Sinopec’s forecast, and a 79% chance that it will be greater than Yakov & Partners’ forecast in 2035.

India’s coal consumption

The story is similar for forecasts on India’s coal consumption. The IEA forecasts India consuming 1,129 Mt of coal in 2026, while Swift Centre forecasters think there is a 99% chance the total amount will be greater than that, with their median figure being 1,508 Mt (34% greater).

Yakov & Partners also published forecasts for Indian coal consumption in their report, including for the years 2030 and 2035 (the probability we assign to coal consumption being less than or equal to these figures are given in parentheses):

2030: 1,346 Mt (2%)

2035: 1,470 (17%)

What drives forecasters’ views here?

Both countries are building more coal power plants

A straightforward way to gauge a potential decrease in coal consumption is by examining whether a country is reducing its coal power generation capabilities. Several forecasters pointed out that both China and India are acting to increase their ability to generate energy from coal.

As data scientist Hannah Ritchie explains, it is possible for countries like China to build more coal plants while simultaneously reducing its coal consumption. As low-carbon energy sources continue to grow, coal power in China is likely to take on the role of ‘peaker plants’, providing flexible generation when needed rather than serving as the baseload of the energy system. This can be seen in the capacity factor (the percentage of time a plant is running at maximum power) of China's coal plants dropping over the last 15 years, from around 70% in the early 2000s to about 50% currently. Therefore, China's coal use could fall despite adding more capacity.

While possible, China are building coal plants at a far higher rate than they would need to if this were the plan. China revived previously cancelled and shelved projects and approved brand-new ones, according to Global Energy Monitor’s Global Coal Plant Tracker. In 2023, they added almost 50,000 MW and retired less than 4,000 MW of productive capacity.

India, meanwhile, has ambitious plans to double energy production by 2030, the vast majority of which is intended to be coal-fired. In 2024, they’re pushing to add 13.9 GW of capacity — the highest annual increase in at least six years.

With clear, articulated plans to increase the use of coal in both countries, it seems implausible that either has reached ‘peak coal’.

Neither China nor India has sufficient sources of clean energy

While China has made huge investments in renewable technologies, they are nowhere near transitioning to a much cleaner energy portfolio over the next decade. Dispatchable energy is required to completely replace coal, but China’s renewable portfolio leans heavily on solar power. Solar power currently accounts for approximately 20% of China's total installed capacity but, in 2022, solar energy only generated around 2.5% of China's total consumption. Additionally, our forecasters stated that the economics of solar power still do not make it a competitive choice:

Although headline cost figures appear favourable, the practicality of energy economics reveals that energy needs to be available at the right time, and storage costs remain prohibitively high.

The story is similar for wind power. Our forecasters also didn’t consider breakthroughs in storage and battery technology to be a big factor in their uncertainty, as they consider it unlikely to make solar energy scalably cost-competitive within the next decade.

Looking at other renewables, low rain in 2023 meant that China’s hydroelectric power capabilities were dampened — another reason that coal usage increased substantially — and the unreliability of rain means that hydroelectric, while considered ‘dispatchable’, is difficult to rely on. Some forecasters noted that heavy rainfall is expected in 2024, which would increase China’s hydroelectric generation in place of additional coal power this year.

A key point driving forecasters’ expectations was the lack of investment in nuclear power.

Look at all the nuclear power plants under construction right now: they amount to a measly 30 GW, while they have a coal generating capacity of around 1100 GW. Clearly, nuclear power isn’t going to replace coal anytime soon.

Overall, the situation is even clearer in the case of India, as it both its economy and population are growing more quickly, and because it is not yet wealthy enough to afford to decarbonise. India has also been phasing natural gas out in recent years — despite it being less polluting — while continuing to rely on coal. (India has much less natural gas in its proved reserves than Russia, China, and the US have.)

Additionally, while India is expanding renewable production alongside coal production, political incentives to bring down rates of power outages ahead of the general election mean that cheap, dispatchable energy sources are required.

Indian economic growth is particularly coal-hungry

Barring unexpected global events, India is likely to maintain a high rate of population and economic growth, which puts serious pressure on their energy production. One forecaster pointed to this when highlighting where they disagree with the IEA’s forecasts:

Economic growth will probably be much higher than the IEA assumes, closer to a 6.5% compound annual growth rate (CAGR), which will require more coal being burned in the short term. The IEA’s 3.5% CAGR of coal seems far too low, with the Indian state itself expecting coal production growth of 6-7% and the potential for imports to grow total usage above this. For reference, power consumption was up by over 8% in 2023.

For an economy like India’s, a high rate of growth will require a high increase in the supply of energy in tandem. Additionally, India’s population is unlikely to peak in the next decade, which means that we’re likely to continue to see increasing energy demands during our forecast period. In the face of an energy-hungry, industrialising, and still-growing India, it appears unrealistic that coal use will fall imminently.

Chinese growth is slower, but still reliant on coal

The story is a bit more complicated in China, a country that has passed peak population and is facing economic turbulence. However, our expert forecasters believe that the conclusions are not too different. While the population has peaked, electricity demand has not. China will also face more energy demand for electric vehicles which hydroelectric and nuclear energy will be too slow to meet. The transition towards electric vehicles will substitute oil consumption with electricity demand, partially driven by coal. While pollution in urban environments may fall, emissions from coal power plants are likely to increase.

Looking at the economy, a slowdown in demand due to a shaky property market has created a fall in demand for steel, which is a major driver of coal usage. If this were to continue, then China might plausibly use less coal going forward. However, some envisage this being offset by an increase in military production and a post-Covid return to normalcy of movement.

As China’s economy matures technologically, some believe it may naturally shift away from coal. While the correlation between economic growth and coal consumption will weaken, there remains a clear and consistent relationship between economic growth and increasing coal usage. One forecaster brought it back to the main observation we are seeing with China’s energy system:

China plans to increase its coal plant capacity by a third. Why would they do this if they did not expect a significant increase in demand?

Summary

Industrial forecasts of India and China’s coal usage over the next decade are incredibly optimistic. Our consensus of our forecasters is that both countries’ coal usage is currently rising, and our aggregate estimates of coal usage over a 1-year, 5-year, and 10-year timeline are between 10% and 50% higher than other sources. India and China’s continued investment in coal power plants, energy-hungry economies, and lack of scalable, cost-competitive alternatives will cause them to rely on coal for longer than many anticipate.

I agree, particularly with India, coal consumption is likely to continue growing. Th IEA has made similar projects for the past decade and they've all been wrong.